Blog

A deep-dive into a variety of pension topics to help you understand and learn more about your pension and the Scheme.

Our blogs will give you information, tips, insights and guidance to help you get to know your pension and support you on your journey to retirement.

<p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> </span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">So you’ve made the decision to retire. And now, after years, or even decades of saving, you’re ready to claim your Industry-Wide Defined Contribution (IWDC) pension.</span><br></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">Thanks to pension freedoms introduced by the Government in 2015, there are more ways than ever for members of a defined contribution (DC) scheme, like the IWDC section, to take their pension savings.</span><br></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">But with great choice, comes great responsibility.</span><br></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">The money you’ve built up in the IWDC section is known as your Personal Retirement Account (PRA). And how you choose to take that money can have a huge impact not only on how much you get, but on how much you have to pay in terms of fees and tax.</span><br></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">So let’s look at your options…</span><br></p><h2><span style="background-color: rgba(0, 0, 0, 0); color: var(--color-h2); font-family: inherit; font-size: var(--font-size-h2); text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">What you can do with your PRA</span><br></h2><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You have 3 main ways to take your PRA as a member of the IWDC section:</span><br></p><ol><li>Get a flexible income, taking it a bit at a time. This is known as drawdown </li><li>Get a regular, secure income, known as an annuity</li><li>Take all of the money in your PRA as a cash lump sum. We call this total encashment</li></ol><p>You can see a summary of your primary options, and how they differ in the table below. </p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You can also read about each option in more detail using the relevant link here</span><br></p><ul><li><a href="/iwdc-members/im-planning-to-take-my-iwdc-pot/understanding-drawdown" target="_blank">Drawdown</a></li><li><a href="/iwdc-members/im-planning-to-take-my-iwdc-pot/understanding-annuities">Annuity</a> </li><li><a href="/iwdc-members/im-planning-to-take-my-iwdc-pot/understanding-encashment">Encashment</a></li></ul><p>The RPS doesn’t currently offer an annuity or drawdown option directly, so to access these you would need to transfer your PRA to another provider.</p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">Options other than the 3 listed above may also be available in line with pension freedoms, however these are not currently offered in partnership with the RPS.</span><br><br></p><table style="border: 1px dotted rgba(0, 0, 0, 1)"><tbody><tr><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><strong>Drawdown</strong> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><strong>Annuity</strong> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><strong>Encashment</strong> </td></tr><tr><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><strong>What is it?</strong></td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)">A drawdown is basically a flexible income. Your PRA remains invested in funds specifically designed for that purpose. And you take out cash whenever you want to, up until your PRA runs out.<br> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)">An annuity is a policy that you buy using money from your PRA. It then guarantees you an income for the rest of your life. Or for a set period of time if it’s fixed term. </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)">Encashment basically means taking all of your PRA as a cash lump sum. </td></tr><tr><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><strong>What are the benefits?</strong> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><ul><li>Flexibility with how/when to take your money</li><li>An opportunity for the value that remains invested to go up</li><li>The ability to withdraw less if you’re coming close to a tax threshold</li><li>Money left in your pot can go to your spouse or dependants if you die</li><li>You can change to an annuity or another product at any time if you wish</li><li>The Trustee is partnering with Legal and General Investment Management (LGIM) to offer members access to its flagship product, the Retirement Income Multi Asset (RIMA) Fund, with preferential fees. See <a href="https://www.legalandgeneral.com/workplace/campaigns/rps-pas/" target="_blank" data-sf-ec-immutable="" data-sf-marked="">Legal & General</a> for details<br></li></ul> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><p>Depending on what type you choose, an annuity could give you:<br></p><ul><li>A guaranteed income for life, or a set period of time</li><li>Income for your spouse or dependents, even if you die </li></ul></td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)">Instant access to all of the savings in your PRA </td></tr><tr><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><strong>What are the risks?</strong> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><ul><li>The value of the money that remains in your PRA can go down</li><li>You may pay a higher rate of tax if you take out a large amount</li><li>If you take any money above your tax-free allowance (25% of your pot), your annual tax allowance could also reduce (as this triggers the Money Purchase Annual Allowance – MPAA)</li><li>Your pot could run out before you die</li><li>The income and additional features you receive, and the fees you need to pay, can vary widely from provider to provider. There may also be different qualifying criteria in place. <br></li></ul> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><ul><li>You need to buy an annuity using money from your PRA, so this reduces your pot initially</li><li>The income you receive can depend on which provider you use and what type of annuity you opt for</li><li>Once you’ve purchased an annuity, it’s very difficult to change your mind, or to adjust your choices, even if your circumstances change</li><li>Providers often charge an administration fee or other management fees for providing an annuity</li><li>The income and additional features you receive, and the fees you need to pay, can vary widely from provider to provider. There may also be different qualifying criteria in place</li><li>If you choose a fixed income annuity, you may find your money doesn’t go as far once inflation rates rise<br></li><li>If you choose a fixed term annuity, this could run out before you die<br></li><li>The terms offered by your annuity provider could appear to lose their value over time </li></ul></td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><ul><li>The money could run out before you die</li><li>Any amount above your tax-free allowance (25% of your pot) may be taxed<br></li><li>You may pay a higher rate of tax if you take out a large amount</li><li>Withdrawing large amounts of cash may affect your eligibility for some Government benefits</li><li>Taking a large cash lump sum puts you at greater risk of scams</li><li>You will not have any remaining funds to provide a regular income for your spouse or any other dependants after you die </li></ul></td></tr></tbody></table><p> </p><p>Whichever option you choose, you could decide to take up to 25% of your PRA as a tax-free lump sum. </p><img src="https://cdn3.railpen.com/mp-sitefinity-prod/images/default-source/old-site-images/avc-extra-link-images/ifgfx_dc_drawdown-pros-and-cons_v01-pra.jpg?sfvrsn=c2b0f48e_1" alt=""><p><br></p><p>It may also be possible to mix and match your options, with a combination of cash, annuity and drawdown if you wish. To do so you would need first select a primary option (drawdown, annuity or encashment) and then take the necessary steps, for example:</p><ul><li>If you take total encashment from the RPS you can then use your cash to buy an annuity or drawdown arrangement </li><li>If you set up an annuity, you can ask the provider to put some of your benefits into a drawdown arrangement </li><li>If you set up a drawdown arrangement, you can ask the provider to put some of your benefits into an annuity </li></ul><p>For both drawdown and annuity you would need to discuss this with your new provider and it would only happen after your entire PRA had transferred out of the Scheme.</p><h2>Tax and other things to keep in mind </h2><p>Before you jump straight in and start claiming your pension, there are a couple of things you may want to bear in mind. </p><p><strong>1. The tax implications</strong><strong> </strong></p><p>Depending on how you access your PRA there may be a limit on how much you can keep saving in your pension before paying tax. This is known as the Money Purchase Allowance (MPAA).</p><p>It is usually triggered if:</p><ul><li>you cash in a pension pot worth more than £10,000</li><li>take your pot through a flexi access drawdown</li><li>use your pot to purchase a fixed term annuity</li></ul><p>Where the MPAA is triggered, it means that the most you can pay into your DC pot in the future is currently £4,000 pa. </p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">This could be particularly problematic if you plan to continue paying in or leave part of your pot invested such as with drawdown.</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">For more information about the MPAA check out our </span> <a href="https://cdn3.railpen.com/mp-sitefinity-prod/docs/default-source/rayn/guides-for-all-members/annual-allowance-tax-limits.pdf?sfvrsn=d6e4ef2d_18" style="font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal" target="_blank">Read As You Need Guide.</a><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> </span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"><strong>2. </strong></span><strong>You</strong><strong style="background-color: rgba(0, 0, 0, 0); color: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> can hold off taking your pension if you prefer</strong></p><p><strong style="background-color: rgba(0, 0, 0, 0); color: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></strong><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">If you’re not quite ready to start taking your pension, then you don’t have to.</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You can delay taking your benefits right up to the age 75.</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">On the plus side, this may give time for your benefits to increase, however there are still risks involved. For example the value of your PRA can go down, as well as up.</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You can find out more about all your options, including what happens if you’re not ready to take your benefits, in the </span>

<a href="/iwdc-members/im-planning-to-take-my-iwdc-pot/how-i-can-take-my-iwdc-pot" target="_blank">how I can take my IWDC pot</a><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> section of this website.</span></p><h2><span style="background-color: rgba(0, 0, 0, 0); color: var(--color-h2); font-family: inherit; font-size: var(--font-size-h2); text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">Making the right decision for you</span></h2><p><span style="background-color: rgba(0, 0, 0, 0); color: var(--color-h2); font-family: inherit; font-size: var(--font-size-h2); text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You can see a summary of your retirement options as a member of the IWDC section in a </span> <a href="/knowledge-hub/help-and-support/video-library">short video</a><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">.</span>

<span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> You can also read about them in more detail in the </span> <a href="/iwdc-members/im-planning-to-take-my-iwdc-pot" style="font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal">planning to take my IWDC pot</a>

<span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> section of the website.</span>

</p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">A range of planning tools are then available within your </span>

<a href="https://member.railwayspensions.co.uk/login" data-sf-ec-immutable="" style="font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal">myRPS </a><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">account to help you consider these options and what might work best for you. This includes a </span>

<strong style="background-color: rgba(0, 0, 0, 0); color: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">retirement modeller</strong><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">, showing what your pension might be worth when you retire and the different ways you can choose to use that money.</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You may also want to speak to an Independent Financial Adviser (IFA).</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">Liverpool Victoria (LV) has been chosen as the official partner to give RPS members access to financial advice. LV can be contacted on 0800 023 4187. </span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You are still free to choose your own Independent Financial Adviser (IFA). You can find an IFA in your area at </span>

<a href="https://www.unbiased.co.uk/" target="_blank" data-sf-ec-immutable="" style="font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal">unbiased.co.uk</a>

</p><h2><span style="background-color: rgba(0, 0, 0, 0); color: var(--color-h2); font-family: inherit; font-size: var(--font-size-h2); text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">What happens once you’ve made a decision</span></h2><p><span style="background-color: rgba(0, 0, 0, 0); color: var(--color-h2); font-family: inherit; font-size: var(--font-size-h2); text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">Once you’ve made your decision and are ready to take your PRA, you need to </span>

<a href="https://member.railwayspensions.co.uk/knowledge-hub/help-and-support/get-in-touch" data-sf-ec-immutable="" style="font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal" data-sf-marked="">contact the Scheme administrator</a><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">, Railpen.</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">The information you need to provide, and the process involved in the next stages, will differ depending on whether you’ve chosen drawdown, annuity or encashment. </span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">Find out more in</span> <a href="/iwdc-members/im-planning-to-take-my-iwdc-pot/applying-to-take-my-iwdc-pot">applying to take my IWDC pot</a><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">.</span>

<span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span></p>

<p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> </span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">So you’ve made the decision to retire. And now, after years, or even decades of saving, you’re ready to claim your Industry-Wide Defined Contribution (IWDC) pension.</span><br></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">Thanks to pension freedoms introduced by the Government in 2015, there are more ways than ever for members of a defined contribution (DC) scheme, like the IWDC section, to take their pension savings.</span><br></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">But with great choice, comes great responsibility.</span><br></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">The money you’ve built up in the IWDC section is known as your Personal Retirement Account (PRA). And how you choose to take that money can have a huge impact not only on how much you get, but on how much you have to pay in terms of fees and tax.</span><br></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">So let’s look at your options…</span><br></p><h2><span style="background-color: rgba(0, 0, 0, 0); color: var(--color-h2); font-family: inherit; font-size: var(--font-size-h2); text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">What you can do with your PRA</span><br></h2><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You have 3 main ways to take your PRA as a member of the IWDC section:</span><br></p><ol><li>Get a flexible income, taking it a bit at a time. This is known as drawdown </li><li>Get a regular, secure income, known as an annuity</li><li>Take all of the money in your PRA as a cash lump sum. We call this total encashment</li></ol><p>You can see a summary of your primary options, and how they differ in the table below. </p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You can also read about each option in more detail using the relevant link here</span><br></p><ul><li><a href="/iwdc-members/im-planning-to-take-my-iwdc-pot/understanding-drawdown" target="_blank">Drawdown</a></li><li><a href="/iwdc-members/im-planning-to-take-my-iwdc-pot/understanding-annuities">Annuity</a> </li><li><a href="/iwdc-members/im-planning-to-take-my-iwdc-pot/understanding-encashment">Encashment</a></li></ul><p>The RPS doesn’t currently offer an annuity or drawdown option directly, so to access these you would need to transfer your PRA to another provider.</p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">Options other than the 3 listed above may also be available in line with pension freedoms, however these are not currently offered in partnership with the RPS.</span><br><br></p><table style="border: 1px dotted rgba(0, 0, 0, 1)"><tbody><tr><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><strong>Drawdown</strong> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><strong>Annuity</strong> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><strong>Encashment</strong> </td></tr><tr><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><strong>What is it?</strong></td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)">A drawdown is basically a flexible income. Your PRA remains invested in funds specifically designed for that purpose. And you take out cash whenever you want to, up until your PRA runs out.<br> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)">An annuity is a policy that you buy using money from your PRA. It then guarantees you an income for the rest of your life. Or for a set period of time if it’s fixed term. </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)">Encashment basically means taking all of your PRA as a cash lump sum. </td></tr><tr><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><strong>What are the benefits?</strong> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><ul><li>Flexibility with how/when to take your money</li><li>An opportunity for the value that remains invested to go up</li><li>The ability to withdraw less if you’re coming close to a tax threshold</li><li>Money left in your pot can go to your spouse or dependants if you die</li><li>You can change to an annuity or another product at any time if you wish</li><li>The Trustee is partnering with Legal and General Investment Management (LGIM) to offer members access to its flagship product, the Retirement Income Multi Asset (RIMA) Fund, with preferential fees. See <a href="https://www.legalandgeneral.com/workplace/campaigns/rps-pas/" target="_blank" data-sf-ec-immutable="" data-sf-marked="">Legal & General</a> for details<br></li></ul> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><p>Depending on what type you choose, an annuity could give you:<br></p><ul><li>A guaranteed income for life, or a set period of time</li><li>Income for your spouse or dependents, even if you die </li></ul></td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)">Instant access to all of the savings in your PRA </td></tr><tr><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><strong>What are the risks?</strong> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><ul><li>The value of the money that remains in your PRA can go down</li><li>You may pay a higher rate of tax if you take out a large amount</li><li>If you take any money above your tax-free allowance (25% of your pot), your annual tax allowance could also reduce (as this triggers the Money Purchase Annual Allowance – MPAA)</li><li>Your pot could run out before you die</li><li>The income and additional features you receive, and the fees you need to pay, can vary widely from provider to provider. There may also be different qualifying criteria in place. <br></li></ul> </td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><ul><li>You need to buy an annuity using money from your PRA, so this reduces your pot initially</li><li>The income you receive can depend on which provider you use and what type of annuity you opt for</li><li>Once you’ve purchased an annuity, it’s very difficult to change your mind, or to adjust your choices, even if your circumstances change</li><li>Providers often charge an administration fee or other management fees for providing an annuity</li><li>The income and additional features you receive, and the fees you need to pay, can vary widely from provider to provider. There may also be different qualifying criteria in place</li><li>If you choose a fixed income annuity, you may find your money doesn’t go as far once inflation rates rise<br></li><li>If you choose a fixed term annuity, this could run out before you die<br></li><li>The terms offered by your annuity provider could appear to lose their value over time </li></ul></td><td style="width: 25%; border: 1px dotted rgba(0, 0, 0, 1)"><ul><li>The money could run out before you die</li><li>Any amount above your tax-free allowance (25% of your pot) may be taxed<br></li><li>You may pay a higher rate of tax if you take out a large amount</li><li>Withdrawing large amounts of cash may affect your eligibility for some Government benefits</li><li>Taking a large cash lump sum puts you at greater risk of scams</li><li>You will not have any remaining funds to provide a regular income for your spouse or any other dependants after you die </li></ul></td></tr></tbody></table><p> </p><p>Whichever option you choose, you could decide to take up to 25% of your PRA as a tax-free lump sum. </p><img src="https://cdn3.railpen.com/mp-sitefinity-prod/images/default-source/old-site-images/avc-extra-link-images/ifgfx_dc_drawdown-pros-and-cons_v01-pra.jpg?sfvrsn=c2b0f48e_1" alt=""><p><br></p><p>It may also be possible to mix and match your options, with a combination of cash, annuity and drawdown if you wish. To do so you would need first select a primary option (drawdown, annuity or encashment) and then take the necessary steps, for example:</p><ul><li>If you take total encashment from the RPS you can then use your cash to buy an annuity or drawdown arrangement </li><li>If you set up an annuity, you can ask the provider to put some of your benefits into a drawdown arrangement </li><li>If you set up a drawdown arrangement, you can ask the provider to put some of your benefits into an annuity </li></ul><p>For both drawdown and annuity you would need to discuss this with your new provider and it would only happen after your entire PRA had transferred out of the Scheme.</p><h2>Tax and other things to keep in mind </h2><p>Before you jump straight in and start claiming your pension, there are a couple of things you may want to bear in mind. </p><p><strong>1. The tax implications</strong><strong> </strong></p><p>Depending on how you access your PRA there may be a limit on how much you can keep saving in your pension before paying tax. This is known as the Money Purchase Allowance (MPAA).</p><p>It is usually triggered if:</p><ul><li>you cash in a pension pot worth more than £10,000</li><li>take your pot through a flexi access drawdown</li><li>use your pot to purchase a fixed term annuity</li></ul><p>Where the MPAA is triggered, it means that the most you can pay into your DC pot in the future is currently £4,000 pa. </p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">This could be particularly problematic if you plan to continue paying in or leave part of your pot invested such as with drawdown.</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">For more information about the MPAA check out our </span> <a href="https://cdn3.railpen.com/mp-sitefinity-prod/docs/default-source/rayn/guides-for-all-members/annual-allowance-tax-limits.pdf?sfvrsn=d6e4ef2d_18" style="font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal" target="_blank">Read As You Need Guide.</a><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> </span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"><strong>2. </strong></span><strong>You</strong><strong style="background-color: rgba(0, 0, 0, 0); color: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> can hold off taking your pension if you prefer</strong></p><p><strong style="background-color: rgba(0, 0, 0, 0); color: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></strong><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">If you’re not quite ready to start taking your pension, then you don’t have to.</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You can delay taking your benefits right up to the age 75.</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">On the plus side, this may give time for your benefits to increase, however there are still risks involved. For example the value of your PRA can go down, as well as up.</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You can find out more about all your options, including what happens if you’re not ready to take your benefits, in the </span>

<a href="/iwdc-members/im-planning-to-take-my-iwdc-pot/how-i-can-take-my-iwdc-pot" target="_blank">how I can take my IWDC pot</a><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> section of this website.</span></p><h2><span style="background-color: rgba(0, 0, 0, 0); color: var(--color-h2); font-family: inherit; font-size: var(--font-size-h2); text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">Making the right decision for you</span></h2><p><span style="background-color: rgba(0, 0, 0, 0); color: var(--color-h2); font-family: inherit; font-size: var(--font-size-h2); text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You can see a summary of your retirement options as a member of the IWDC section in a </span> <a href="/knowledge-hub/help-and-support/video-library">short video</a><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">.</span>

<span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> You can also read about them in more detail in the </span> <a href="/iwdc-members/im-planning-to-take-my-iwdc-pot" style="font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal">planning to take my IWDC pot</a>

<span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> section of the website.</span>

</p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">A range of planning tools are then available within your </span>

<a href="https://member.railwayspensions.co.uk/login" data-sf-ec-immutable="" style="font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal">myRPS </a><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">account to help you consider these options and what might work best for you. This includes a </span>

<strong style="background-color: rgba(0, 0, 0, 0); color: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">retirement modeller</strong><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">, showing what your pension might be worth when you retire and the different ways you can choose to use that money.</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You may also want to speak to an Independent Financial Adviser (IFA).</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">Liverpool Victoria (LV) has been chosen as the official partner to give RPS members access to financial advice. LV can be contacted on 0800 023 4187. </span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">You are still free to choose your own Independent Financial Adviser (IFA). You can find an IFA in your area at </span>

<a href="https://www.unbiased.co.uk/" target="_blank" data-sf-ec-immutable="" style="font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal">unbiased.co.uk</a>

</p><h2><span style="background-color: rgba(0, 0, 0, 0); color: var(--color-h2); font-family: inherit; font-size: var(--font-size-h2); text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">What happens once you’ve made a decision</span></h2><p><span style="background-color: rgba(0, 0, 0, 0); color: var(--color-h2); font-family: inherit; font-size: var(--font-size-h2); text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">Once you’ve made your decision and are ready to take your PRA, you need to </span>

<a href="https://member.railwayspensions.co.uk/knowledge-hub/help-and-support/get-in-touch" data-sf-ec-immutable="" style="font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal" data-sf-marked="">contact the Scheme administrator</a><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">, Railpen.</span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">The information you need to provide, and the process involved in the next stages, will differ depending on whether you’ve chosen drawdown, annuity or encashment. </span></p><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">Find out more in</span> <a href="/iwdc-members/im-planning-to-take-my-iwdc-pot/applying-to-take-my-iwdc-pot">applying to take my IWDC pot</a><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">.</span>

<span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span></p>

So you’ve made the decision to retire. And now, after years, or even decades of saving, you’re ready to claim your Industry-Wide Defined Contribution (IWDC) pension.

Thanks to pension freedoms introduced by the Government in 2015, there are more ways than ever for members of a defined contribution (DC) scheme, like the IWDC section, to take their pension savings.

But with great choice, comes great responsibility.

The money you’ve built up in the IWDC section is known as your Personal Retirement Account (PRA). And how you choose to take that money can have a huge impact not only on how much you get, but on how much you have to pay in terms of fees and tax.

So let’s look at your options…

You have 3 main ways to take your PRA as a member of the IWDC section:

You can see a summary of your primary options, and how they differ in the table below.

You can also read about each option in more detail using the relevant link here

The RPS doesn’t currently offer an annuity or drawdown option directly, so to access these you would need to transfer your PRA to another provider.

Options other than the 3 listed above may also be available in line with pension freedoms, however these are not currently offered in partnership with the RPS.

| Drawdown | Annuity | Encashment | |

| What is it? | A drawdown is basically a flexible income. Your PRA remains invested in funds specifically designed for that purpose. And you take out cash whenever you want to, up until your PRA runs out. | An annuity is a policy that you buy using money from your PRA. It then guarantees you an income for the rest of your life. Or for a set period of time if it’s fixed term. | Encashment basically means taking all of your PRA as a cash lump sum. |

| What are the benefits? |

| Depending on what type you choose, an annuity could give you:

| Instant access to all of the savings in your PRA |

| What are the risks? |

|

|

|

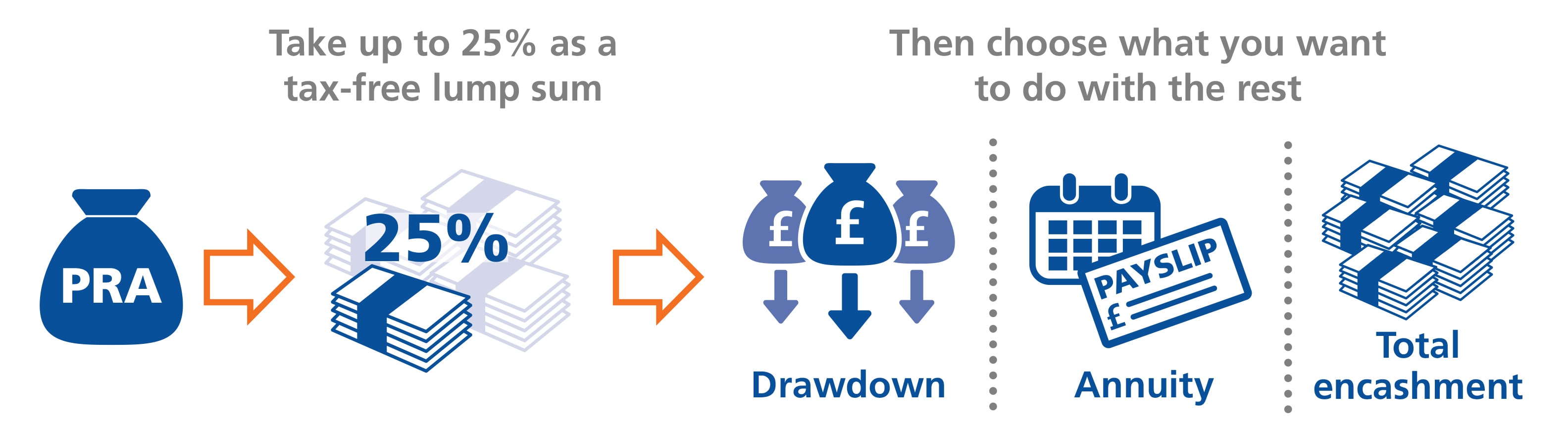

Whichever option you choose, you could decide to take up to 25% of your PRA as a tax-free lump sum.

It may also be possible to mix and match your options, with a combination of cash, annuity and drawdown if you wish. To do so you would need first select a primary option (drawdown, annuity or encashment) and then take the necessary steps, for example:

For both drawdown and annuity you would need to discuss this with your new provider and it would only happen after your entire PRA had transferred out of the Scheme.

Before you jump straight in and start claiming your pension, there are a couple of things you may want to bear in mind.

1. The tax implications

Depending on how you access your PRA there may be a limit on how much you can keep saving in your pension before paying tax. This is known as the Money Purchase Allowance (MPAA).

It is usually triggered if:

Where the MPAA is triggered, it means that the most you can pay into your DC pot in the future is currently £4,000 pa.

This could be particularly problematic if you plan to continue paying in or leave part of your pot invested such as with drawdown.

For more information about the MPAA check out our Read As You Need Guide.

2. You can hold off taking your pension if you prefer

If you’re not quite ready to start taking your pension, then you don’t have to.

You can delay taking your benefits right up to the age 75.

On the plus side, this may give time for your benefits to increase, however there are still risks involved. For example the value of your PRA can go down, as well as up.

You can find out more about all your options, including what happens if you’re not ready to take your benefits, in the how I can take my IWDC pot section of this website.

You can see a summary of your retirement options as a member of the IWDC section in a short video. You can also read about them in more detail in the planning to take my IWDC pot section of the website.

A range of planning tools are then available within your myRPS account to help you consider these options and what might work best for you. This includes a retirement modeller, showing what your pension might be worth when you retire and the different ways you can choose to use that money.

You may also want to speak to an Independent Financial Adviser (IFA).

Liverpool Victoria (LV) has been chosen as the official partner to give RPS members access to financial advice. LV can be contacted on 0800 023 4187.

You are still free to choose your own Independent Financial Adviser (IFA). You can find an IFA in your area at unbiased.co.uk

Once you’ve made your decision and are ready to take your PRA, you need to contact the Scheme administrator, Railpen.

The information you need to provide, and the process involved in the next stages, will differ depending on whether you’ve chosen drawdown, annuity or encashment.

Find out more in applying to take my IWDC pot.

22/6/2021

Editorial

<p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">As an IWDC member, you can choose not only how and when you want to retire, but how your money is invested in the meantime.</span> <span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> </span> </p><p>All of this can have a real effect on how much you end up with, so it’s worth taking the time to get to know your pension and make sure you have all the information you need to make the right decisions for you. <br></p><p>Here’s a few things to look out for: </p><h2><strong style="background-color: rgba(0, 0, 0, 0); color: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto; font-size: inherit">1. Your investment funds</strong></h2><p>As an IWDC member, the money you pay into your pension (known as contributions) is invested in a variety of specially selected funds.<strong style="background-color: rgba(0, 0, 0, 0); color: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto; font-size: inherit"> </strong></p><p>You can choose these funds for yourself, or take a more hands-off approach and have them managed for you by the Scheme’s investment manager, RPMI.<span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> </span></p><p>If you decide to manage the funds yourself, there are five ‘self-select’ funds to choose from, each with different levels of risk. <span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> </span></p><p>If you would prefer to have the funds managed for you, then you will be invested into a Lifestyle Strategy. This means your investments will automatically change over time as you move towards your retirement.<span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> </span></p><p>Either way, it’s important to keep an eye on your funds and consider regularly whether they still meet your needs. <span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> </span></p><p>For example, if you have just joined the Railways Pension Scheme and don’t plan to retire soon, you may want to take more risks for higher returns. </p><p> If you are getting closer to retirement, you may have a more cautious approach to investments and opt for more ‘stable’ funds which have a lower risk of losing value. </p><p>More information about all of the fund options available can be found <a href="/iwdc-members/managing-investments/fund-choices">here<span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> </span></a></p><p>And you can review your investment funds at any time by logging in to your <a href="https://member.railwayspensions.co.uk/login" data-sf-ec-immutable=""></a><a href="https://member.railwayspensions.co.uk/login" data-sf-ec-immutable="">myRPS account</a> <br></p><h2><strong>2. Your Target Retirement Age</strong><br><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"></span></h2><p><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto">If you’re invested in one of the lifestyle strategies mentioned above you can choose a Target Retirement Age (TRA). </span><br></p><p>This sets the age at which you hope to stop work. And it’s important because it affects the way your investments are handled. </p><p>Ten years before your TRA, your contributions will be automatically moved into investment funds that are deemed more stable. While these funds may grow at a smaller rate, they should protect your Personal Retirement Account (PRA) from any sudden changes in the market and, in particular, from any losses you wouldn’t have time to recoup. </p><p>Your TRA can be anywhere between 55 and 75 years old, or from age 50 if you have a Protected Pension Age. </p><p>It can be checked and changed at any time, by logging in to your <a href="https://member.railwayspensions.co.uk/login" data-sf-ec-immutable=""></a><a href="https://member.railwayspensions.co.uk/login" data-sf-ec-immutable="">myRPS account</a>t </p><p>Once logged in you can also use the retirement modeller to see what impact changing your TRA could have on your pension overall. </p><h2><strong>3. Your savings </strong></h2><p>You can check how much is in your PRA at any time by logging in to your <a href="https://member.railwayspensions.co.uk/login" data-sf-ec-immutable=""></a><a href="https://member.railwayspensions.co.uk/login" data-sf-ec-immutable="">myRPS account</a> </p><p>Once logged in you can also use our retirement modeller to see what your PRA might be worth by the time you retire. </p><p>If you’re not sure whether it’s going to be enough, then you can use our <a href="/knowledge-hub/help-and-support/retirement-budgeting-calculator">retirement budgeting calculator</a> to work out how much it might cost to get the retirement lifestyle you want, and compare the two. </p><p>More information about getting your savings on track can be found <a href="/iwdc-members/im-planning-to-take-my-iwdc-pot/how-much-ill-need">here</a></p><p>And if you’re still paying in to your IWDC pension, you can find more details about how to boost your PRA through Additional Voluntary Contributions (AVCs) <a href="/iwdc-members/Im-still-working/saving-more">here</a> </p><h2><strong>4. Your helping hand</strong><br></h2><p>Before making any changes to your IWDC pension, you may wish to get independent financial advice. <br></p><p>Liverpool Victoria (LV) has been chosen as the official partner to give RPS members access to financial advice. LV can be contacted on 0800 023 4187. </p><p>You are still free to choose your own Independent Financial Adviser (IFA). You can find an IFA in your area at <a href="https://www.unbiased.co.uk/" target="_blank" style="font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto" data-sf-ec-immutable=""></a><a href="https://www.unbiased.co.uk/" target="_blank" data-sf-ec-immutable="">unbiased.co.uk.</a><span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> </span></p><p>You can find out more about your retirement options as an IWDC member in the RPS <a href="/iwdc-members/im-planning-to-take-my-iwdc-pot/how-i-can-take-my-iwdc-pot">here<span style="background-color: rgba(0, 0, 0, 0); color: inherit; font-family: inherit; font-size: inherit; text-align: inherit; text-transform: inherit; white-space: inherit; word-spacing: normal; caret-color: auto"> </span></a></p><p>You can also get general pensions information and guidance through<a href="https://www.moneyhelper.org.uk/en/pensions-and-retirement/" target="_blank" data-sf-ec-immutable=""> </a><a href="https://www.moneyhelper.org.uk/en/pensions-and-retirement/" data-sf-ec-immutable=""></a><a href="https://www.moneyhelper.org.uk/en/pensions-and-retirement/" data-sf-ec-immutable="">MoneyHelper</a> </p>

There are so many things in life that are out of our control – but your pension doesn’t have to be one of them.

Read the latest updates from the world of pensions and see how they affect you as a member of the Scheme.

We provide regular newsletters to help you navigate your pension whether you're paying into the Scheme, not paying in anymore, or receiving your pension.

Register with Platform today to have your say in how we communicate with you and other members about your pension.

Railways Pensions is powered by Railpen Limited

© Railpen Limited 2010-2025. Registered Office: 100 Liverpool Street, London EC2M 2AT

Each of Railpen Limited (registered in England and Wales No. 2315380) and Railway Pension Investments Limited (RPIL) (Registered in England and Wales No. 1491097) is a wholly owned subsidiary of Railways Pension Trustee Company Limited (Registered in England and Wales No. 2934539). Registered office for each company: 100 Liverpool Street, London EC2M 2AT. RPIL is authorised and regulated by the Financial Conduct Authority for some of its activities. The administration of occupational pension schemes is not a regulated activity. Full details about the extent of RPIL's authorisation and regulation by the Financial Conduct Authority are available from us on request.